As a small business owner, you might sometimes need extra money to keep things running smoothly. Merchant cash advances (MCAs) are a fast way to get funds for your business. Unlike regular bank loans, MCAs are paid back through a portion of your future sales, often from credit card transactions.

However, MCAs don’t offer the same benefits and protections as traditional small business loans. Their high fees and complex contracts can put your business at risk if you’re not careful. If you think you might default on an MCA, it’s important to understand how this could affect your business.

Let’s go over what happens if you default on a merchant cash advance, how you can avoid it and what steps to take if you’re already falling behind on payments.

How Merchant Cash Advances Work

A merchant cash advance (MCA) gives businesses quick access to money by allowing them to sell a portion of their future sales to the lender at a discount. Businesses that often use MCAs are those needing cash fast and have steady sales or many credit card transactions. It’s important to remember that an MCA isn’t a loan, it’s an advance on future sales.

Here’s how it works: A business applies for an MCA by sharing its sales records and other necessary documents. The lender reviews the business’s sales history and cash flow to decide if they qualify and how much money they can get. If approved, the business receives a lump sum payment.

Repayment is based on how much the business earns in sales, with the lender taking a percentage of daily or weekly sales, known as the “holdback” rate. If the business makes a lot of sales, repayment happens faster, if sales are slow, repayment slows down too. Instead of interest rates, MCAs use “factor rates” which are numbers like 1.1 to 1.5. This number helps calculate how much the business will need to repay in total.

Why Merchant Cash Advances Are Different

Unlike other types of small business loans, dealing with a merchant cash advance (MCA) can be more challenging if things go wrong.

Many MCA contracts include something called a “confession of judgment.” When you sign a contract with this clause, you’re basically giving up your right to defend yourself if the lender claims you broke the agreement. This means the lender can file a lawsuit and get a judgment against you without giving you a chance to fight it. They can then start seizing your business assets through legal means such as UCC liens, to get their money back.

Additionally, most MCA providers require a personal guarantee. This means that if your business can’t repay the advance, the lender can come after your personal assets as well. So, if a lawsuit happens, it could affect not just your business but also your personal finances.

Here’s an Example of Merchant Cash Advance

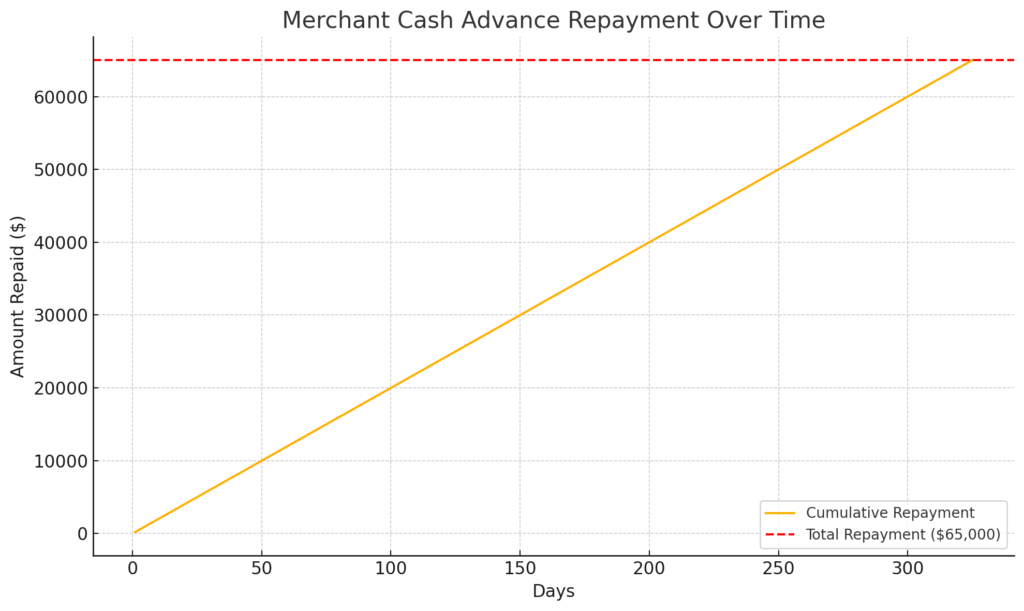

Let’s say a restaurant needs to renovate its kitchen quickly and decides to get a merchant cash advance to cover the cost. The lender approves an advance of $50,000 with a factor rate of 1.3.

- Advance Received: $50,000

- Factor Rate: 1.3

- Total Repayment: $50,000 * 1.3 = $65,000

The agreement states that the lender will take 10% of the restaurant’s daily credit card sales until the full $65,000 is repaid. If the restaurant makes about $2,000 in credit card sales each day, the daily repayment would be $200 (10% of $2,000). If sales stay consistent, it would take around 325 days to repay the advance. However, the actual time could change depending on how much the restaurant earns in daily sales.

While merchant cash advances can be a flexible option for businesses with strong sales but less-than-perfect credit, they are more expensive than traditional loans. So, it’s important to be cautious before taking this type of funding.

Defaulting on a Merchant Cash Advance: What Happens Next?

If you miss one or more payments on a merchant cash advance (MCA), it’s considered a default which is a breach of contract. Here’s what could happen if you default:

- Intense collection efforts: The MCA provider may aggressively try to collect the money you owe. This could involve hiring collection agencies or taking legal steps to enforce repayment.

- Legal action: If the MCA provider sues and wins, they can get a court judgment against your business. If there’s a personal guarantee involved, they might also come after your personal assets. This could result in your bank accounts being frozen or assets being seized to pay off the debt.

- Personal financial risk: Many MCA contracts include a personal guarantee. This means that if your business can’t repay, you might have to use your personal savings or property to settle the debt.

- Credit score impact: While MCAs usually don’t show up on credit reports (because they’re not traditional loans), defaulting can still hurt your personal credit score and your business’s creditworthiness especially if there’s a court judgment involved. This could make it harder to get future financing.

- Damage to your reputation: Legal problems and financial difficulties can harm your business’s reputation with customers, suppliers and partners. This can affect your business’s future growth and success.

- Challenges in renegotiation: Some MCA providers might be willing to adjust the repayment terms if you’re struggling but not all are flexible. If you default, it could make it harder to negotiate and you might end up with stricter terms that put even more strain on your business.

What Is an MCA Lawsuit?

When an MCA (merchant cash advance) company sues a customer, they first send a court summons and a complaint notice. This document explains why they’re suing you and gives you a deadline to respond with a formal legal answer. The time you have to reply depends on where you live. For example, in New York, you have 20 days if the notice is handed to you in person and 30 days if it’s sent by mail.

It’s very important to respond before the deadline. If you don’t, the MCA company can get a default judgment against you, meaning you lose the right to challenge or defend yourself in the lawsuit.

Some MCA contracts include a “confession of judgment” clause. This allows the MCA company to skip the regular legal process. They can get a judgment against you without notifying you or giving you a chance to defend yourself in court. After that, they can quickly seize your business assets, freeze your accounts and more.

Additionally, many MCA contracts include a personal guarantee. This means that if your business can’t pay the debt, you are personally responsible for it. In a lawsuit, your personal assets and money could be at risk too.

Steps You Can Take to Defend Yourself

While a confession of judgment limits your options, it’s not always unbeatable. In some states, you might be able to challenge it if you can prove any of the following:

- The confession of judgment doesn’t follow state law or local rules.

- The details in the confession of judgment such as the people involved or the amount owed, are incorrect.

- Your breach of contract doesn’t meet the conditions necessary to trigger the confession of judgment.

- The lender didn’t clearly explain what the confession of judgment meant when you signed the contract.

If you think any of these apply to your situation, you might be able to ask the court to cancel the confession of judgment. If you’re dealing with legal problems related to an MCA, it’s a good idea to get help from a lawyer who can guide you through the process.

Tips to Avoid Defaulting on a Merchant Cash Advance

Defaulting on a merchant cash advance (MCA) can have serious consequences for your business and personal finances. It can lead to legal problems, hurt your credit score and even put your personal assets at risk. If you think you might struggle to make payments, it’s important to take steps to avoid defaulting. Here are a few things you can do:

Look for Ways to Cut Costs

Since MCA payments are tied to your sales, they can really cut into your cash flow. One way to free up some money is by reducing expenses within your business. Consider hiring freelancers or contractors to save on labor costs or renting equipment instead of buying it outright. You could also try negotiating with your vendors or suppliers to get better rates and lower your expenses.

Try to Restructure the Debt

If you think you’re going to have trouble making your MCA payments, reach out to the MCA Company as soon as possible. While these companies can be difficult to deal with, they might be willing to adjust the terms if it means they’ll keep getting paid. You might be able to negotiate a short break in payments (forbearance) to help your finances recover.

Many MCA contracts have a clause called reconciliation or readjustment. If your business income drops, it might be impossible to make payments as originally agreed. In that case, the MCA company is required to restructure the payments to make them more manageable, otherwise they could be seen as engaging in illegal lending practices.

Consider Debt Consolidation

If you’re looking to get out of your MCA agreement, one option is debt consolidation. This means taking out a loan with set monthly payments and using the money to pay off the MCA. Instead of daily payments tied to your sales, you’ll have a fixed monthly payment over several years. The interest rate is usually lower, especially if you have good credit which helps when applying for a traditional business loan. Overall, the terms of a term loan are more favorable compared to an MCA.

Attempt to Settle the Debt

You could also try to settle the debt by negotiating with the lender to agree on a lump sum that’s less than the total amount you owe. It’s best to work with a debt settlement attorney who understands how MCA companies operate. They can negotiate for you and help handle the tricky parts of the settlement process.

Get a Business Credit Card

If MCA debt is leaving you with tight cash flow, getting a business credit card might help. You can use the card to cover important expenses when cash is low and then pay off the balance when you have more funds. Just be sure to manage your payments carefully and avoid letting the balance grow or you could end up with even more debt on top of your MCA troubles.

Hire a Debt Relief Lawyer for Help

If you’re worried about falling behind on MCA payments, defaulting on a merchant cash advance or even facing a lawsuit, hiring an MCA debt settlement lawyer is crucial. An experienced lawyer can help review your situation and develop a plan that allows your business to continue running while dealing with aggressive debt collectors and MCA companies.

These attorneys are skilled in negotiating business debt settlements which could help reduce the amount you owe. They often have relationships with merchant cash advance companies and their legal teams, giving them insight into the legal processes that may impact your business. Your priority should be running your business, while a legal team can handle the complex world of MCA debt resolution. The stress of dealing with MCA debt and other business challenges can be overwhelming but having the right legal support can help you achieve the best possible outcome for your business.

FAQs

What are merchant cash advance direct lenders?

Merchant cash advance (MCA) direct lenders are companies that provide businesses with upfront capital in exchange for a portion of future sales. They operate without intermediaries or brokers.

What happens in a merchant cash advance lawsuit?

In a merchant cash advance lawsuit, the lender may sue a business for defaulting on payments. The lawsuit could result in asset seizure or other legal actions to recover the owed amount especially if there’s a personal guarantee involved.

Can I get a merchant cash advance with no credit check?

Yes, some MCA providers offer funding without a credit check but they often rely on your business’s sales history to determine eligibility instead of traditional credit scores.

What do merchant cash advance brokers do?

Merchant cash advance brokers act as middlemen between businesses and MCA lenders. They help find the right lender and terms for businesses looking to secure quick funding.

Can I get a merchant cash advance with bad credit?

Yes, MCAs are available to businesses with bad credit since they are based on future sales rather than traditional creditworthiness.

What does a merchant cash advance attorney do?

An MCA attorney helps businesses deal with legal issues related to merchant cash advances including debt settlement, contract disputes and defense against lawsuits.

What is merchant cash advance consolidation?

MCA consolidation involves taking out a single loan to pay off multiple merchant cash advances, often with more favorable repayment terms and lower interest rates.

How does merchant cash advance debt relief work?

MCA debt relief involves strategies such as debt settlement, consolidation or restructuring to reduce the financial burden on businesses struggling with multiple MCA obligations.

Should I hire a merchant cash advance lawyer?

If you’re facing legal issues related to MCA debt such as a lawsuit or difficulties with repayment, a merchant cash advance lawyer can help negotiate settlements, handle legal disputes and protect your business.

What are the legal issues surrounding merchant cash advances?

Legal issues related to MCAs often involve breach of contract, personal guarantees and confession of judgment clauses that allow lenders to take swift legal action if a business defaults on payments.

You May also like: Prince Narula Digital PayPal A Game-Changer in Finance